"Britcoin" is a Non-Solution to an Imaginary Problem

"Britcoin" is a Non-Solution to an Imaginary Problem

Ditto da dubious digital dollar

It seems like lately, governments around the world are falling over themselves to create various types of government-backed digital currencies. It’s not much of a surprise that these “experts” in finance don’t understand why crypto exists in the first place — and therefore make promises that don’t make sense or are impossible to fulfill.

But before we go over why the “experts” are wrong to push their digital currencies, let’s go over the basics of crypto currencies and why they exist. In no particular order, here are the most important aspects of any good digital currency:

1 — Decentralization. Unlike fiat currencies such as the dollar, nobody controls the supply of bitcoin and therefore nobody can decide to “print” more and devalue the bitcoin currently in circulation. There’s no “emergency” printing to bail out failing financial institutions. That directly leads into the next point……

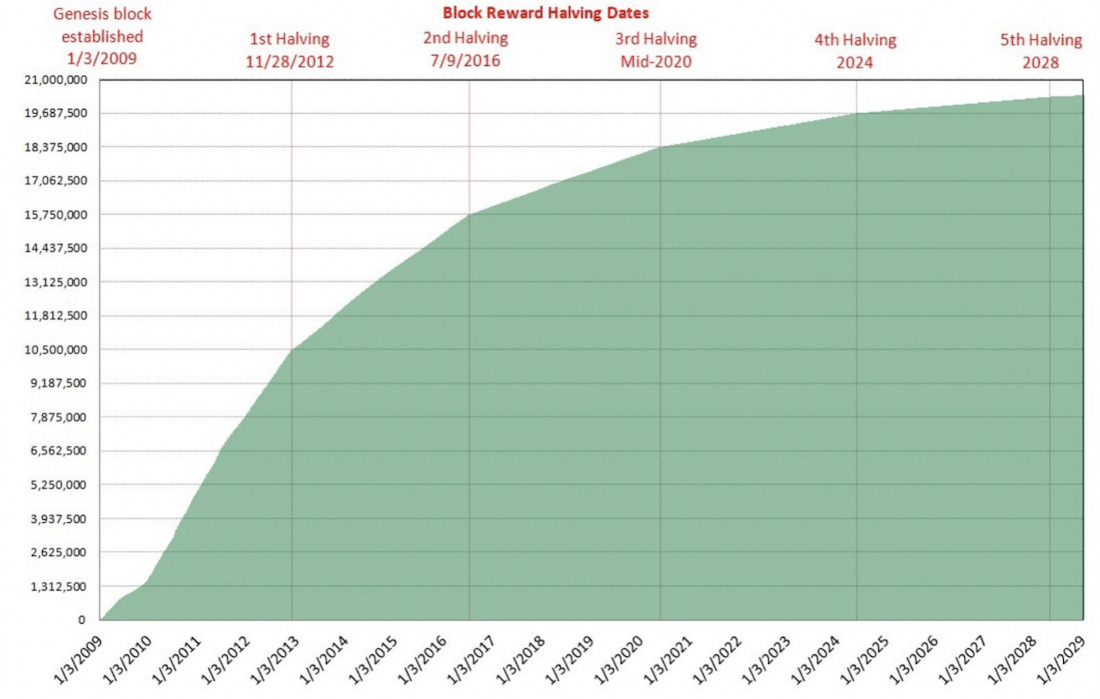

2 — Predictable supply. With good crypto, we know exactly how many units will be in the total supply, and we know roughly when the last one will be mined. This allows us to predict what the “money” supply will be at any point until then:

How many dollars will be in existence in 2025? 2030? 2050? Nobody has any clue, because the supply of dollars is determined by a group of bankers and politicians — who always find an excuse to print more cash and pass it off to their well-connected buddies. This is vitally important because the dollar is half of every transaction we make.

3 — Permissionless transactions. As more and more customers are finding out these days, payment processors are increasingly playing the role of financial police, shutting down “unapproved” accounts or fundraisers — even when those fundraisers are quite obviously legal. And since you don’t know what activity will retroactively be placed on the “unapproved” list, there’s an obvious benefit to permissionless transfers.

4 — Crypto doesn’t require a bank. Billions of people have no access to banking services, but DO have access to phones. (Somewhat surprisingly, 6% of American adults have no bank account at all!) Crypto allows these people to participate in the modern economy and does so without enriching the banks at all. (Bonus!)

5— Small transaction fees. Remittance companies such as Western Union typically charge $10 or more to transfer money overseas. And we send A LOT of money overseas:

If you’re keeping track at home, $74,577 million is $74.5 BILLION dollars sent overseas from the US ALONE in 2021. If we use the 7.14% figure as a baseline, that’s just over $5 BILLION in fees! Use of crypto would leave the bulk of that $5 billion in the hands of the people sending or receiving it.

6 — (For retailers) No chargebacks. If you’ve spent any time in business at all, you’ve had to deal with slimeballs who use the internal policies of companies like PayPal to their advantage. Perhaps the most common scam involves placing a huge order, and once it arrives simply claiming it never showed. As a policy, Paypal sides with buyers, and business owners are out of luck if they run into one of these scammers. (It’s fair to note that by using crypto, the risk in these cases shifts back to the buyer, it doesn’t disappear.)

7 — (For buyers) No exposure to credit card/bank account information. At this point, I think we’ve ALL gotten some variation of the email that says “Due to a data breach…….”. Centralized databases are ripe for malfeasance. With crypto, your “wealth reserves” are never in danger when you use your wallet to make a purchase — because your cards/bank account are never a factor in the transaction.

There are seven solid positives of crypto. And (surprise!) getting rich by HODLING doesn’t even make an appearance (with the possible exception of #5, which is really more about protecting wealth from the falling value of the dollar). In fact, I must be a Terrible Libertarian because the main positives revolve around helping the lowest people on the totem pole by allowing them access to the modern economy without enriching the already filthy-rich banks and governments. (Remember when the left hated banks? Good times.)

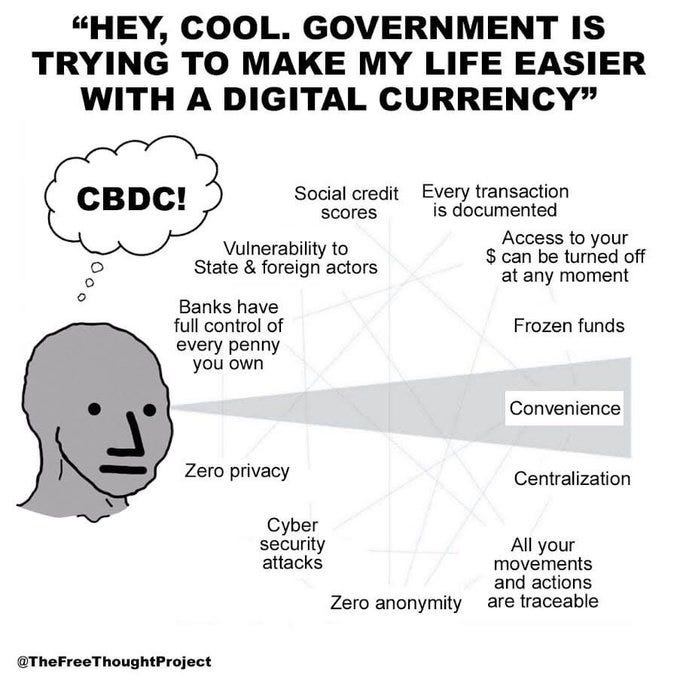

Now, let’s run down this list as it pertains to government-run cryptos. First, it’s important to note that the most common acronym for these projects is “CBDC” — which stands for “Central Bank Digital Currency.”

Well, that immediately destroys crypto positive #1.

1 — Decentralization. We want to END the Fed, not give it another way to screw us over! Why would we trust the same people who are ruining the real economy to try to run a digital one? (We shouldn’t)

Let’s go down the rest of our list of positives and see how many still pertain to a CBDC.

2 — Predictable supply. Because the value of an American CBDC is tied to the dollar, it doesn’t really matter how many “Digital Dollars” are in existence — the more relevant metric is how many “Digital Dollars” are in existence PLUS how many “Actual Dollars” are in existence. (And we already know we have no idea about future dollar supply.) Since the Digi Dollar is pegged to the Actual Dollar, it loses value at the same rate —that’s obviously not going to protect anybody from the dollar’s devaluation.

3 — Permissionless transactions. One of the stated goals of CBDCs is to enable crackdown on financial crime. (Though the idea that criminals would start using a CBDC for crimes is a little wacky to begin with.) If you think you’re going to be able to send your digital currency for an “unapproved” use (such as online poker or purchase of a firearm), I’ve got a bridge to sell you.

4 — Crypto doesn’t require a bank. While currently used CDBCs in Nigeria and the Eastern Caribbean Currency Union don’t require a bank account, they DO require some sort of identification verification before users are allowed into the system. My suspicion is that “modern” countries such as the US will require digital wallets to be tied to traditional bank accounts — giving hackers and scammers another point of attack. (More on that later!)

5 — Small transaction fees. In a world in which Americans have multiple ways to send dollars online FOR FREE, any sort of transaction fee will likely be seen as too much. Because we’re not sure how other countries would handle our CBDC, we don’t really know if this is an improvement over the current system when sending money overseas. It’s possible that retailers could see some sort of reduction in fees if they use CBDCs over debit/credit cards, but that remains to be seen. (And I bet Visa has something to say about the matter.)

6 — (For retailers) No chargebacks. One of the “advantages” of a centralized system is that somebody has control over it — meaning somebody has the ability to reverse transactions. This means retailers will simply trade “Paypal overlords” resolving disputes to “government overlords” resolving disputes. Hard pass.

7 — (For buyers) No exposure to credit card/bank account information. It’s possible that this positive will remain intact, but as I say above, I expect government to at least attempt to tie your digital wallet to your real-life banking information. Obviously, that would completely negate this positive.

With CBDCs, we’ve reduced our list of positives from seven to……….what? One and a half (4, some of 5)? Possibly we retain up to three of them? (4/5/7?)

This is yet another example of government touching something and turning it to crap — and we haven’t even gotten into the REAL downsides of taking away those decentralization positives and handing control to government:

When we take a step back and really look at the situation, handing over your money to a bank is actually kind of insane. You’re basically saying “Here’s almost all my wealth, please don’t lose it.” It’s doubly insane to turn it over to a bank like Silicon Valley Bank, which is busy funding any impossible Green Dream ever conceived. But since SVB knows that the taxpayers will bail it out once the bets go bad, the system continues to roll on — kicking the can down the road. And since now banks can fail at basically any time, the “experts” conclude that digital currency can “protect” consumers. (Personally, I’d be focusing on the fact that our financial system is so unsustainable that bank runs are a thing, but that’s just me!)

See, when your bank gets caught lying about how much money they actually have and you can’t actually access your cash, you’ll be protected because you have some digital currency that has a value tied to the currency that was just exposed as an elaborate lie!

Protection!

Oh, and there’s also this:

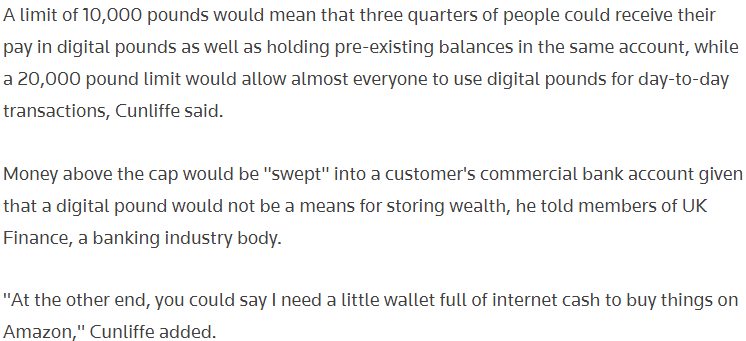

First — note the casual linkage here between your digital wallet and your bank account. This is why I think your online wallet will be tied to a bank account — they tell us so.

Second, £20,000 is roughly $25,000. How long would $25,000 last you if you had no access to your regular bank? Would you even be able to withdraw that money in the event of a banking run, or would you be locked out of your own account (for the greater good, of course)? Do we really think this is about protection when your bank goes under? (I sure hope not!)

And WHY do you need a little wallet full of internet cash to buy things on Amazon in the first place? Are current Amazon payment options lacking in England? If so, why not expand those options instead of creating a CBDC? (Hint: It’s because the CBDC isn’t about buying stuff on Amazon.)

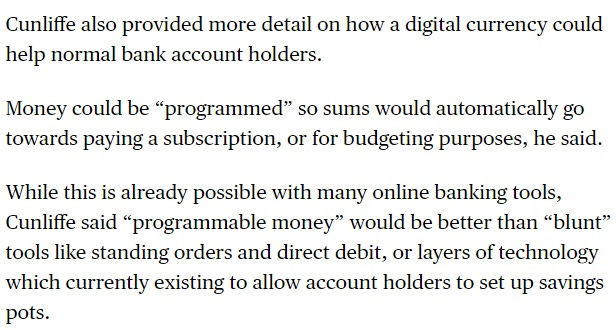

Do you see what he’s really saying? Read it again, slowly.

If you didn’t see it — let me repeat the important part after a terrible bit of adjustment in MS Paint:

That’s what this is really all about. It’s not about your convenience, and it’s not about helping out the little people. This is the currency portion of the control crisis, where they attempt to take control over the entire financial system and use it as the most powerful sledgehammer in history. The money can be “programmed” to leave your account to pay what the government says you owe — and who controls if and when that happens? It certainly won’t be you.

Perhaps the only positive with CBDCs is that they will be run by government and therefore probably not even function to begin with. It’s the thinnest of silver linings.

I want to note that there are TONS of crappy cryptos out there (shitcoins) -- and most of them are worthless because they stray from what makes a "good" currency to begin with. When discussing "good" crypto, I'm basically talking Bitcoin/Ethereum/Monero and a scant few others that have actual real-world uses.

Great silver lining, actually! The chances they'll f****this up are at least 50%.